Whether you're covering an emergency expense, funding a major purchase, consolidating debt, or pursuing an important life goal, a personal loan can help bridge the gap. But approval isn't guaranteed—and getting approved starts long before you submit an application.

Understanding how lenders assess borrowers can help you prepare more effectively, avoid unnecessary rejections, and choose a loan that fits your financial situation. In this guide, we'll walk you through practical steps to strengthen your application and move forward with confidence.

12 Personal Loan Tips to Help Improve Your Application in the Philippines

Want to know how to get approved for a personal loan? Check this list first before submitting that application.

1. Borrow an Amount You Can Comfortably Repay

Before applying for a personal loan, take a close look at your finances and determine how much you truly need to borrow. While a larger loan amount may seem appealing, it's important to consider how the monthly repayments will fit into your budget.

One way to assess your borrowing capacity is by calculating your debt-to-income (DTI) ratio. The debt-to-income ratio compares an individual’s monthly debt payment to his or her monthly gross income.[1]

How to Compute Debt-to-Income Ratio

To calculate your debt-to-income ratio, simply divide your monthly total debt payment by your monthly gross income and then multiply the amount by 100.

Debt-to-income ratio = (Monthly total debt payment ÷ Monthly gross income) x 100

For example, if your monthly gross income is ₱25,000, and your monthly total debt payment is ₱10,000, your debt-to-income ratio is 40%. This means you spend 40% of your salary on monthly debt payments.

In general, a lower DTI ratio indicates greater financial flexibility and may improve your chances of loan approval. More importantly, it helps ensure that your loan remains manageable and doesn't interfere with other financial goals, such as building an emergency fund, saving for a major purchase, or planning for future milestones.

2. Understand the Types of Personal Loans Available

Learn about the types of personal loans in the market. You can get a secured or an unsecured personal loan, but what is the difference?

A secured loan requires collateral, such as a vehicle, property, or another valuable asset. Because the lender has added security, secured loans may offer higher loan amounts and lower interest rates.

However, it's important to understand the risks. If you're unable to meet your repayment obligations, the lender may have the right to repossess the asset used as collateral.

With an unsecured loan, you don’t have to put up collateral, making them a popular option for borrowers who don't want to pledge assets. However, because lenders take on more risk, these loans may come with lower borrowing limits and higher interest rates.

While your assets aren't directly at risk, missed payments can still affect your credit history and make it more difficult to qualify for future financial products.

When deciding between secured and unsecured loans, consider not only the cost of borrowing but also your repayment capacity and overall financial circumstances.

3. Compare Personal Loans

Many financial institutions in the Philippines offer personal loans, so it can get overwhelming. Do your research first, so you know your options—this is one of the most important personal loan tips.

According to the Bangko Sentral ng Pilipinas, borrowers consider the interest rate, loan amount, repayment period, and easy loan application when applying for a loan. Consider these factors as well when comparing loan products.

Beyond interest rates, consider factors such as:

- Processing and service fees

- Eligibility requirements

- Approval and disbursement timelines

- Overall affordability

Apart from these, consider your loan needs and how much you can afford. Banks won’t loan you an amount you can’t pay. So, when comparing different loan providers, ensure that the interest rate, processing fees, and loan term are realistic in relation to your financial standing.

Read more: How to Compare Personal Loans

Check Out Personal Loans from Top Providers in the Philippines

|

Metrobank

|

4. Talk to Various Lenders

Get in touch with lenders to know more about their loan products. You may call their customer service hotlines or inquire via email.

You can also head to your local bank and ask questions about the personal loan application process, time frame, terms, additional fees, and repayment schemes. This will help you fully understand the loan you’re trying to apply for.

Too busy to call or visit multiple lenders? Make your search for the best personal loan in the Philippines a lot easier through Moneymax. Our free comparison platform not only enables you to compare different personal loans but also conveniently apply for a loan.

5. Have Your Personal Loan Application Documents Ready

Before starting the personal loan application process, prepare all the documentation you’ll need. Different financial institutions may have different requirements, so contact your preferred lender ahead of time to get a checklist of the items you need to submit.

You have to submit a fully accomplished personal loan application form, a photocopy of your valid ID, and proof of income. You may have to submit additional document requirements, depending on your lender.

Check your lender’s eligibility requirements as well. Typically, those who are at least 21 years old and Filipino citizens or foreigners permanently residing in the Philippines are eligible for a personal loan. Some lenders may require a minimum gross monthly income for loan applications.

6. Check Your Assets and Liabilities

Assets are things you own such as properties, vehicles, and other investments. Liabilities, on the other hand, are your financial obligations, such as credit cards and mortgages. Lenders may look at these factors when you apply for a loan.

So before applying for a personal loan, check your outstanding liabilities. Having unpaid debt can impact your credit history, affecting how much you can borrow.

7. Improve Your Credit History

Financial institutions look at your credit history to determine whether you are a trusted and disciplined lender. If you pay your credit card balances on time every month, this shows that you can make the monthly payments on your loans.

If you have maintained a credit card with good standing, this shows that you have the discipline to pay off personal loans spanning two or three years.

Here are some ways you can improve your credit history for your personal loan application:

- Pay your bills on time

- Pay your bills in full

- Spend less than your credit limit amount

- Keep old accounts (longevity counts)

- Avoid external factors that impact your history negatively (e.g. foreclosure, bankruptcy, etc.)

8. Make Sure You Have Proof of Income

You have a better chance of loan approval if you’re employed than if you’re a freelancer. The risk for banks is lower because you have a steady flow of income, which means you're financially capable of repaying your loan.

If you’re self-employed, your lender may ask you to provide the following documents:

- A copy of your Income Tax Return (ITR)

- Your audited financial statements for the past years

- Necessary licenses or permits such as a DTI registration certificate or an SEC registration

These documents show that you have a history of earning and paying taxes. Take note of these personal loan tips, whether you're an employee or a self-employed individual.

See also: Loan Options and Approval Tips for Freelancers in the Philippines

_1200x350.png?width=751&height=219&name=UB_PL_Generic_2_(Jan_2025)_1200x350.png)

9. Be a Disciplined Borrower

Financial institutions also decide in favor of borrowers with multiple forms of credit that they repay regularly.

For example, you have three credit cards and a car loan. You pay all your credit card balances and loan amortization on time every month. It shows you can maintain a good credit standing while managing to pay multiple forms of credit.

However, don’t borrow more than you can afford. If you already have multiple forms of credit, but you can barely pay for them, getting a personal loan may not be the best idea.

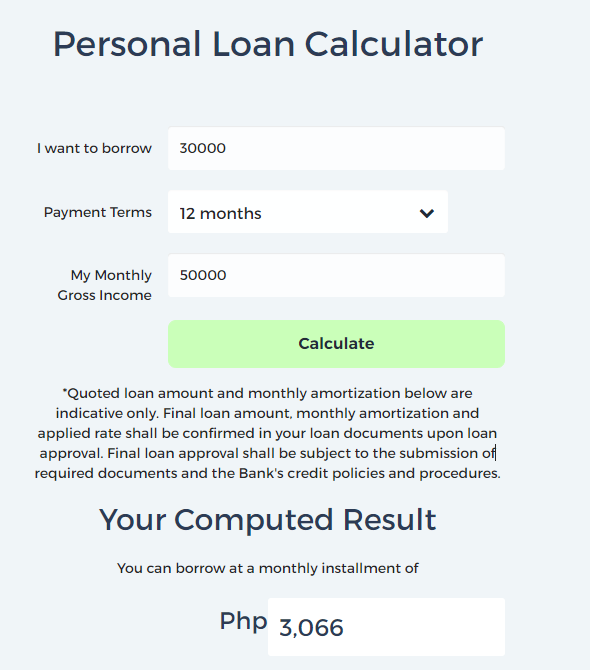

10. Use the Lender’s Loan Calculator

To find out your possible loan interest, monthly installment amount, and fees, use the lender’s loan calculator on its official website.

Here’s a sample from Security Bank’s online loan calculator:[2]

First, enter the amount you wish to borrow. Remember, don't borrow an amount you can't afford to pay or don't need. It’s not practical to pay a loan you won’t even use for your financial need.

Next, choose how long you want to pay for your loan. The loan duration or tenor plays an important role in determining the cost of your personal loan.

Lastly, check your estimated monthly installment.

This loan calculator will show you how much your expected monthly repayment will be. So for this example, you’ll be paying ₱3,066 every month for 12 months for the loan amount of ₱30,000.

At a glance, you can also find out the interest that your loan will incur for one year.

- ₱3,066 x 12 = ₱36,792

- ₱36,792 - ₱30,000 (principal amount) = ₱6,792

In the computation above, you can see that the loan will incur an interest amount of ₱6,792 for one year (or ₱566 each month). This doesn't include late payment fees and other personal loan fees.

11. Improve Your Relationship with the Bank

Having a good relationship with your bank can help it evaluate your creditworthiness. Being a credit cardholder can help, but so can being a long-time client with several bank accounts.

Some banks don't even look at how much you currently have in your accounts. More often, banks will check how long your accounts have been active and in good standing.

12. Know the Difference Between Good Debt and Bad Debt

Making a personal loan means being in debt to the loan provider. As a borrower, check whether you’re signing up for good debt or bad debt.

Good debt involves taking out a loan to fund something that will potentially grow your assets[3] in the long term. Examples of good debts are money spent on tuition fees, career advancement, home renovation, or business capital.

In contrast, bad debt involves borrowing money for something that will potentially reduce or prevent your asset growth. These things depreciate over time, like vehicles, shopping sprees, and unplanned purchases.

So know your goal before taking out a personal loan. This will determine whether it’s a good or bad debt. Borrowing money for something that will not help you gain financially is not practical and may lead to unpaid debt for years.

How to Prepare for a Smoother Personal Loan Application

While approval timelines vary from one lender to another, taking a few steps before you apply can help reduce delays and improve your overall borrowing experience.

- Review your credit standing. Your credit history can influence how lenders assess your application. Before applying, take time to review your credit report and check for any inaccuracies. If your credit score needs improvement, addressing it early may help strengthen your financial profile — not just for this loan application, but for future financial milestones as well.

- Know how you'll receive the funds. Different lenders disburse loan proceeds in different ways. Some release funds through bank transfers or e-wallets, while others may issue checks. Understanding the disbursement process ahead of time can help you avoid delays and plan your finances more effectively.

- Prepare your documents in advance. One of the simplest ways to speed up the application process is to ensure your requirements are complete and up to date. Gather the necessary documents, such as valid IDs, proof of income, and tax records, and double-check that all information in your application is accurate and consistent.

- Understand additional requirements. Some lenders may require a guarantor or co-borrower, particularly for certain loan types or borrower profiles. If this applies to your application, discuss the requirements with your chosen guarantor ahead of time and ensure they can provide the necessary documents.

- Plan your repayment strategy. A personal loan should support your goals—not create financial stress. Before applying, review your budget and determine how the monthly payments will fit into your existing expenses. If possible, identify additional income sources or areas where you can reduce spending to create a comfortable repayment buffer.

If Your Personal Loan Application Is Rejected, Here's What to Do Next

Having a loan application declined can be disappointing, but it doesn't mean the door is permanently closed. In many cases, a rejection simply highlights areas that may need improvement before you apply again. Here are additional personal loan tips to help improve your chances when you apply again:

- Reduce existing debt. Lenders look at your ability to manage additional financial obligations. Paying down credit card balances or existing loans can improve your debt-to-income ratio and strengthen future applications.

- Review your documents. Incomplete, outdated, or inconsistent information can sometimes affect approval decisions. Before reapplying, make sure all documents are accurate, complete, and up to date.

- Explore other financing options. A personal loan may not always be the best or most suitable solution. Depending on your circumstances, you may qualify for a different type of loan or financing product that better matches your needs and financial profile.

- Strengthen your financial position. Consider ways to increase your income, build your savings, or establish a stronger repayment history. Even a few months of consistent financial improvement can make a meaningful difference in future applications.

- Reapply when you're better prepared. Avoid submitting multiple applications immediately after a rejection. Instead, take time to address the factors that may have affected your application and reapply once your financial situation has improved.

Remember: a rejected application isn't necessarily a setback — it's an opportunity to build a stronger financial foundation for your next step.

-png-1.png?width=751&height=219&name=image%20(30)-png-1.png)

Final Thoughts

A personal loan with low interest rate in the Philippines can be a useful financial tool when used thoughtfully and for the right reasons. By understanding how lenders evaluate applications, preparing your finances in advance, and borrowing within your means, you can improve your chances of approval while protecting your long-term financial health.

Whether you're applying for your first loan or exploring your options after a rejection, every financial decision is an opportunity to build a stronger foundation for the goals ahead.

Sources:

- [1] Debt-to-Income (DTI) Ratio (Investopedia, 2022)

- [2] Security Bank Personal Loan Calculator

- [3] Good Debt vs Bad Debt: What’s the Difference? (Investopedia, 2021)

Back to Blog

Back to Blog