It feels exhilarating when summer hits—the endless bright skies brim with promise and possibility. Take this as your cue to fund your summer goals!

Whether you plan to travel overseas, take up a new hobby or passion project, or renovate your house, you can jumpstart your plans with a loan. Read tips on how to manage a personal loan so you can be mindful of your expenses and stay on top of your finances.

8 Tips on How to Manage a Personal Loan

It’s not enough to know how personal loans work. You must learn how to manage them to avoid penalty charges and protect your credit score.

Step 1: Pick a Reputable Lender

-Apr-26-2024-01-06-45-6186-AM.png?width=600&height=400&name=Pics%20for%20blog%20-%20600x400%20(31)-Apr-26-2024-01-06-45-6186-AM.png)

Choose a trusted and reputable loan provider that offers competitive rates and flexible repayment terms. This is crucial in helping you manage your personal loan—a legit lender will not prey on you and take advantage of your financial situation.

So, make sure to compare loan providers and read reviews from other customers who’ve tried their loan products.

Related: How to Compare Personal Loan Rates: Know Which Loan is the Best for You

Step 2: Read the Fine Print

Before signing your loan agreement, read the terms and conditions thoroughly. All that lengthy text can look overwhelming and intimidating, but it’s very important to read it—it will allow you to understand how personal loans are calculated, where additional personal loan fees come from, and how repayments work.

Once you understand these details, you can better manage your loan and avoid unpleasant surprises down the line.

Step 3: Calculate Your Monthly Payments

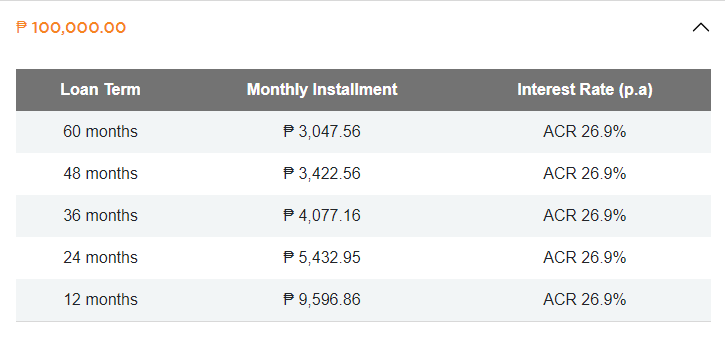

Get insight into what your monthly amortization will look like by checking sample computations. Most banks and financial institutions show sample calculations with personal loan rates on their website. Use their online calculators to get an estimate of monthly payments and the total costs.

For example, let’s say you plan to apply for a UnionBank Personal Loan. Its Personal Loan Repayment Calculator shows sample computations for personal loans ranging from ₱100,000 to ₱2 million.

Check out this example for a loan amount of ₱100,000 and loan terms of 12, 24, 36, 48, and 60 months, based on an average Annual Contractual Rate (ACR) of 26.9%.[1]

Related: Fund Your Big Dreams: How to Apply for a UnionBank Personal Loan

Step 4: Adjust Your Monthly Budget

A personal loan is an added expense. So, before you apply for one, you need to know how it will affect your budget. Assess your income and expenses to know how much you can set aside for your loan without drastically adjusting your budget for essentials.

Divide your expenses into categories to quickly determine which to cut back on or remove. Need help making a budget? Fortunately, there’s an abundance of budgeting apps and free resources online.

Learning how to manage loan repayments will be a walk in the park once your budget is sorted out. You can save money and put it toward loan repayments. If you do this every month, you won’t need to worry about not being able to pay the loan.

While you’re at it, consider setting aside some advance payments if you can. This will ensure you’ll always pay on time.

Step 5: Pay on Time

-Apr-26-2024-01-09-05-8780-AM.png?width=600&height=400&name=Pics%20for%20blog%20-%20600x400%20(32)-Apr-26-2024-01-09-05-8780-AM.png)

When you get approved for a loan, you’re responsible for paying it back on time. Plus, you get to avoid late charges and penalties that quickly add up and make your loan more expensive or challenging to manage.

This also helps improve your credit score, which can help boost your chances of approval when you apply for credit cards or new loans in the future.

Step 6: Set Up Automatic Payments

Never miss a due date by setting up automatic payments for your loan. Get your loan repayments automatically charged on your credit card or debited from your specified bank account. This will save you the trouble of having to remember due dates and making manual monthly payments.

For instance, with a UnionBank Personal Loan, you must agree to an Auto-Debit Agreement before you can receive the loan proceeds. You’ll just have to make sure your UnionBank deposit account contains enough balance.

Step 7: Learn Your Lender’s Policy on Early Repayment

Paying off your loan before the end of the term means you achieve financial freedom sooner.

However, lenders usually have a prepayment clause in their terms and conditions. They will charge an early repayment fee if you pay off your loan ahead of schedule. Therefore, it’s crucial to know the terms and conditions before you pay more than your fixed monthly loan amount.

Step 8: Keep an Eye on Your Credit Score

-Apr-26-2024-01-11-37-1793-AM.png?width=600&height=400&name=Pics%20for%20blog%20-%20600x400%20(33)-Apr-26-2024-01-11-37-1793-AM.png)

As mentioned, the way you manage a personal loan will reflect on your credit score. Keep a close watch on it while repaying your loan—especially if you have multiple.

Lenders look at your credit score when determining your creditworthiness or reliability. Missed payments impact your credit score negatively and make it harder to get approved for higher-tier credit cards and car, home, or business loans.

Further reading: 16 Loans With Easy Application and Approval in the Philippines

-png-1.png?width=751&height=219&name=image%20(30)-png-1.png)

Final Thoughts

Now that you know how to manage a personal loan, go ahead and start fulfilling your summer goals! Get the financial boost you need and fund your big dreams fast by applying for a UnionBank Personal via Moneymax today:

_1200x350.png?width=751&height=219&name=UB_PL_Generic_2_(Jan_2025)_1200x350.png)

DISCLAIMER: This article was created in partnership with UnionBank of the Philippines. While we are financially compensated for this collaboration, we ensure to maintain our editorial integrity to provide you with the best recommendations that can help you make smarter financial decisions.

Source: [1] Annual Contractual Rate (UnionBank)

Back to Blog

Back to Blog