If you’re a hardworking professional, the last thing you want is to get sick and injured—and therefore unable to work and provide for yourself or your loved ones.

Unfortunately, illnesses, accidents, and death can happen at any time. Depending on your situation, it can put a lot of pressure on your finances and derail your life goals.

Fortunately, you can avail of income protection insurance to avoid that scenario. This type of insurance is a financial lifesaver, just like life, personal accident, or health insurance.

What exactly is income protection insurance? Here’s a guide on what it is, how it works, why you should have it, and where to get it.

What is Income Protection Insurance?

You may have heard of it from friends and colleagues. But what’s the meaning of income protection insurance?

As the name suggests, income protection insurance is a type of insurance that gives you a fixed amount of money every month should you find yourself unable to work due to a permanent disability caused by anything, such as an accident. It can help cover expenses like utility bills, credit cards, and home or car loans while you’re unable to work.

The payout is typically 50% to 65% of your monthly income. But ultimately, the salary percentage and the benefit period (the maximum period your policy will pay a monthly benefit) will depend on your insurance provider and income protection plan. Like life insurance, income protection insurance can be tailored to suit your needs.

How Does Income Protection Work?

To start with, it’s different from life or personal accident insurance. While life and personal accident benefits are given as a one-off lump sum, an income protection benefit provides regular income through monthly cash benefits.

The goal of income protection insurance is to take away the financial pressure by replacing lost earnings. It allows you to continue living your current lifestyle and pay for expenses while sidelined. It pays out the income protection benefit until you reach the end of the benefit period.

When you purchase insurance for income protection, you can select the waiting period (the time you must wait before you can file a claim), the benefit period, and the insurable income (the amount of income that will be replaced).

👉 What Does Income Protection Cover?

If you’re considering this type of insurance, you must know what income protection covers. Although income protection insurance covers total disablement that results in your inability to work, it does not cover the following:

- Pre-existing medical or chronic conditions

- Disabilities due to military activities, criminal acts, self-harm/intentional causes, influence of alcohol, or misuse of drugs

- Pregnancy and childbirth

- Elective surgeries and treatments

- Self-administered unemployment

Types of Income Protection Insurance Policies

-Apr-15-2024-10-44-42-7953-AM.png?width=600&height=400&name=Pics%20for%20blog%20-%20600x400%20(1)-Apr-15-2024-10-44-42-7953-AM.png)

Here are the most common types of income protection insurance you can get:

- Short-term income protection insurance - It typically covers five years or less at lower premiums.

- Occupation-specific income protection insurance - This type of policy offers special terms for people with specific occupations at a higher premium.

- Age-banded or reviewable premium - This type of policy regularly adjusts the premiums during the insurance term as you age.

- Guaranteed premium - Your income protection insurance premium won’t increase for the term duration. But you may have to pay higher premiums at the start.

How Much Does Income Protection Insurance Cost?

Now that you know what it is and what types there are, you might wonder how much is income protection per month.

The cost varies depending on several factors, such as your age, medical history, lifestyle, income, and the riskiness of your job. The waiting period, benefit period, and the amount of insurable income also affect the cost.

Who Should Get Income Protection Cover?

-Apr-15-2024-10-46-08-4351-AM.png?width=600&height=400&name=Pics%20for%20blog%20-%20600x400%20(2)-Apr-15-2024-10-46-08-4351-AM.png)

Income protection insurance is a must if:

- You’re the breadwinner responsible for all household expenses and have family members relying on your income

- You’re self-employed or a small business owner who has no sick leaves or vacation leaves

- Your occupation has an increased risk of injury or accident

- You have a mortgage or debts you need to pay regardless of your employment or situation

- You don’t have significant savings or an emergency fund

- You want extra financial protection and peace of mind

So should you get income protection insurance in the Philippines?

If you work in a typically safe environment and don’t get exposed to significant medical risk, you may not see the need for it. But if you want to cover all your bases and stay financially protected, you should avail of income protection insurance.

Paying for groceries, utilities, rent, and mortgage is difficult and stressful when you’re disabled without a regular wage. While you can tap into your savings or emergency fund, will it last you several months or years?

Income protection insurance makes it possible for you to meet your living costs, whether you’re providing for just yourself or an entire family. When you have income insurance protection coverage, you still earn a regular monthly income to pay for your living expenses. Thus, you can use your life savings or emergency fund for their intended purposes.

Read more:

- Should You Get Life Insurance? Consider These 8 Factors

- Starting a Family? Consider These 10 Family Insurance Types

Where to Get Income Protection Insurance

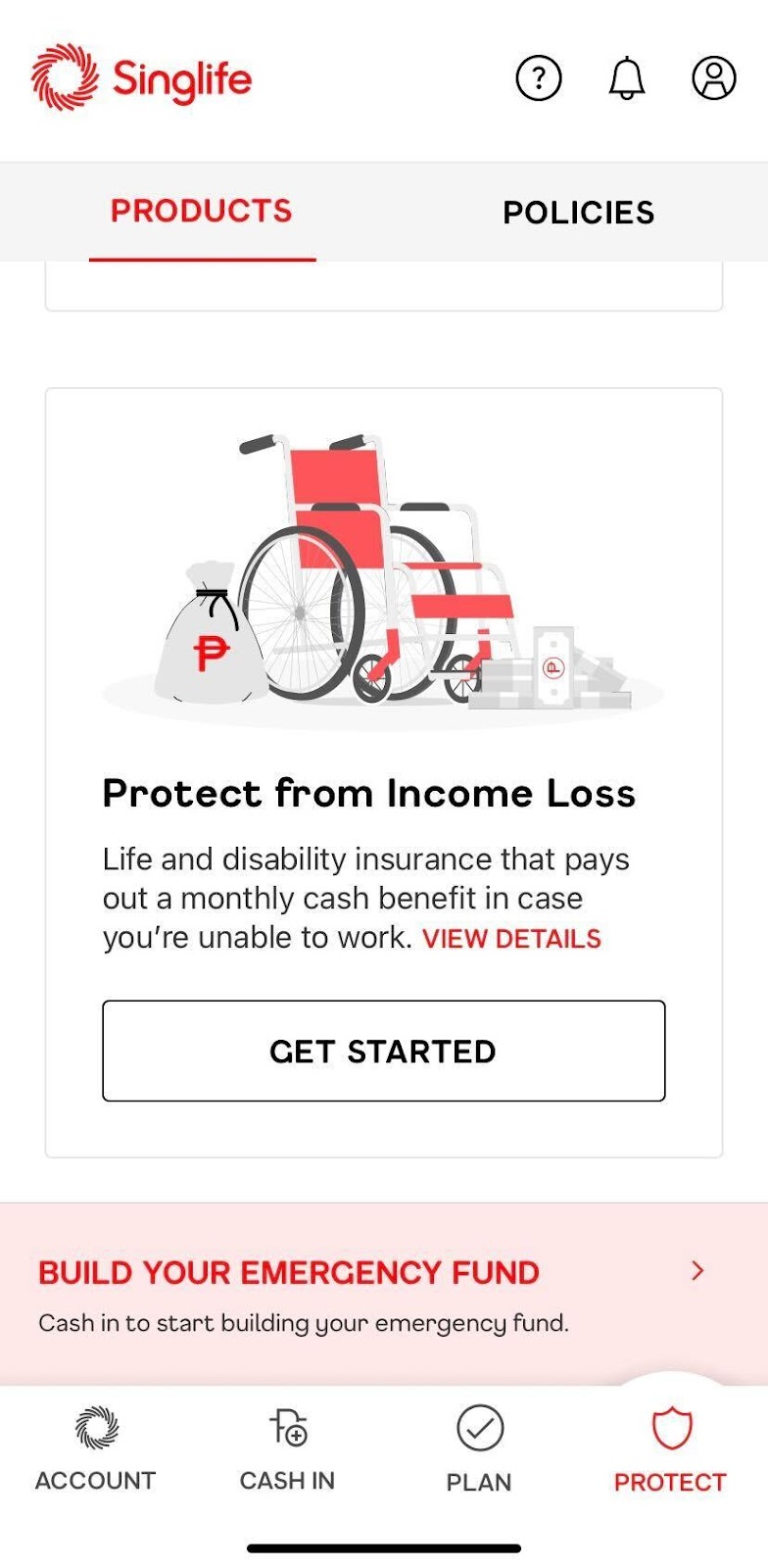

You don’t need to look far (or, in this case, go out of the house) to get the best income protection insurance. Singlife, the first purely digital life insurer in the Philippines, offers an affordable and comprehensive income protection plan called Protect from Income Loss, conveniently available on the Singlife Plan & Protect App.

🛡️ Singlife’s Protect from Income Loss Features

- Wide coverage - Protect from Income Loss covers a wide range of causes, including extreme sports like skydiving, skiing, and paragliding, which aren’t typically covered by other life insurers. You can easily check any exclusions and limitations on the Singlife website.[1]

- Monthly cash payout - Enjoy a monthly cash benefit paid out between one to 10 years for your or your family’s daily expenses. This will give your family a regular income stream. You also have the option to receive a one-off lump sum.

- Quick and convenient - After downloading the Singlife Plan & Protect App, you can get a quote and purchase a policy in minutes—all without having to speak to a financial advisor!

- Cash bonus - Receive a cash bonus on the last monthly payout date.

Read more: Secure Your Future with the Best Life Insurance in the Philippines

🛡️ How to Get Singlife’s Protect from Income Loss

Get a personalized quotation and purchase this policy in minutes on the Singlife Plan & Protect App, the first and only mobile app that helps you save for emergencies, plan your financial goals, and have money for your different needs through life insurance.

- Download the Singlife Plan & Protect App here.

- Create an account.

- Log in to your account. Tap Products under the Protect tab.

- Under Protect from Income Loss, tap Get Started.

- Answer the questions to get recommendations most suited to your budget and needs.

- After tapping Continue, proceed to answer questions about your medical background and work setup.

- Next, review your answers before getting your final quotation.

- Read the quotation carefully, especially the monthly premium and benefits. You can proceed to assign beneficiaries or skip to the confirmation page.

- Review the summary of benefits, monthly premiums, and all the attached declarations and documents. Once done, tick the terms and conditions box and tap the Confirm button.

Related: Take Full Control of Your Financial Future with Moneymax and Singlife Philippines

🎁 Bonus: Get Free Life Insurance from Singlife

_1200x350.png?width=734&height=214&name=Singlife_MOM250_Promo_(May_2024)_1200x350.png)

Until May 30, get free life insurance from Singlife! This comes in the form of ₱251 Singlife Credits, covering death and disability worth up to three months of your declared salary.

Here’s how to avail of the promo:

- After downloading the Singlife Plan & Protect App and creating an account, choose Redeem a Voucher as a cash-in option.

- Enter the code MOM250. Note that you must redeem your free credits within 90 days from receipt of the code.

- Wait for ₱251 to be credited directly to your account.

Use your free credits to get up to three months’ worth of life insurance or buy other products via the Singlife Plan & Protect App. Make sure to grab yours ASAP—limited vouchers are available daily!

Final Thoughts

In these uncertain times, getting a family income protection plan is a must. An income protection insurance policy gives you the peace of mind that you can keep supporting yourself and your loved ones financially if the unexpected happens and you’re left unable to earn income.

And what better way to save, plan, and protect your goals than with a financial partner like Singlife? In the time it takes you to finish reading this article, you can have one less thing to worry about. Purchase income protection insurance on the Singlife Plan & Protect App via the banner below:

_CTA_Banner.png?width=751&height=219&name=Singlife_Main_KV_(Sep_2023)_CTA_Banner.png)

DISCLAIMER: This article was created in partnership with Singlife Philippines. While we are financially compensated for this collaboration, we ensure to maintain our editorial integrity to provide you with the best recommendations that can help you make smarter financial decisions.

Source: [1] What are the accidents not covered?

Back to Blog

Back to Blog