Adulting is both a scary and exciting journey, especially for those who plan to build their credit history and achieve financial independence. For this, credit cards for beginners are among the best financial tools you can use.

Applying for a credit card sounds intimidating and complicated, but fortunately, there are cards for beginners with no credit history yet. These starter credit cards may have low credit limits or limited perks, but they serve their purpose of helping you manage finances better and build credit.

To help you choose your best budgeting and spending partner, here’s what you need to know about credit cards for beginners in the Philippines.

How to Choose a Credit Cards for Beginners: 4 Features to Look for

-Feb-12-2024-04-35-38-0297-AM.png?width=600&height=400&name=Pics%20for%20blog%20-%20600x400%20(11)-Feb-12-2024-04-35-38-0297-AM.png)

Looking for the best credit cards for first-timers? Since this is your first time, let’s trim down your options. Here are the things you should look for when choosing the best credit card for beginners in the Philippines.

🔎 Low Annual Fee

Consider credit cards with annual fees not exceeding ₱3,000 to save money. Ideally, choose one with no annual fees for life.

If you get approved for a card that doesn’t waive the annual membership fee, try to find out how you can waive the fees. Most credit card issuers set conditions for waiving annual fees.

For example, you may need to meet a minimum spend requirement, enroll a biller, or get a supplementary card. Ask your credit card issuer first before submitting your credit card application.

🔎 Low Credit Card Fees

If you're looking for the best credit card for first-timers, focus on the two most common fees: the late payment fee and the overlimit fee.

You get charged an overlimit fee when you spend more than your credit limit, while a late payment fee is charged when your payment is not posted on time. To avoid these fees, pay all your credit card dues on time and keep your credit card usage low.

Other fees you should keep note of include foreign transaction fees (if you’re traveling abroad), annual percentage rates, and balance transfer fees.

🔎 Your Preferred Credit Card Perks

Most credit cards for beginners in the Philippines don't offer as many privileges as premium ones. Still, you can find the best credit cards for starters with perks that appeal to you, whether you want a card with rewards on shopping, travel, dining, or any other spending category.

Online personal finance platforms like Moneymax can also help you assess credit cards based on your needs, according to HSBC Senior Vice President and Head of Marketing Anya Katigbak-Cajucom.

"If you're a beginner, they can provide you with the list of where you can apply for first-timer cards," Anya said. "Having a good relationship with the bank would also weigh in, and it's a big difference when you do have a relationship with the bank. Each bank, depending on the relationship, can provide you with your new card."

Related reading: 15 Thrilling Welcome Gifts for New Credit Cardholders This 2024

🔎 Security Features

When choosing the best credit card for first-timers, find out which bank implements the best security measures. This way, you're assured that there won't be any unauthorized transactions by hackers and scammers using your credit card account.

Some crucial security features to look for include the following:

- Chip technology - An embedded microcomputer technology that stores information and can’t be counterfeited

- Zero Liability Policy - Available in both Mastercard and Visa credit cards. It ensures cardholders will not be responsible for paying fraudulent charges made with their credit card

- Anti-phishing initiatives - Visa's anti-phishing measures encourage cardholders to report emails and websites posing to be connected with Visa

- Identity theft resolution - A measure through which cardholders can easily cancel a compromised credit card

- Account Information Security Program - A program that eliminates unnecessary information and data storage in compliance with the PCI Security Standards Council[1]

- SecureCode - An added security feature at the end of every online transaction that asks for a code to be sent to your mobile number

- Verified by Visa - A global authentication program that lets Visa verify the card user's identity in real-time

- Tokenization - Replaces your Mastercard account number with a token that can be used safely for all contactless payments

16 Best Credit Cards for Beginners in the Philippines

Here's a glance at a few of the top credit cards for newbies:

| Credit Card for First-Timers | Features and Benefits |

|

UnionBank Rewards Credit Card

|

|

|

Metrobank Titanium Mastercard®

|

|

|

Security Bank Gold Mastercard

|

|

|

BPI Rewards Card

|

|

|

BPI Edge Card

|

|

|

PNB Ze-Lo Mastercard

|

|

|

AUB Easy Mastercard

|

|

|

AUB Classic Mastercard

|

|

Know more about these and the rest of the best cards for beginners below.

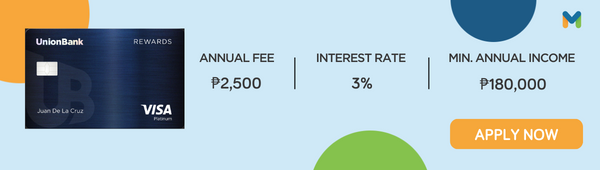

UnionBank Rewards Credit Card

📌 UnionBank Rewards Credit Card Features and Benefits

- 1 never-expiring point for every ₱30 spend

- 3x points when you shop and dine, both here and abroad

💳 UnionBank Rewards Credit Card Fees and Charges

- Annual fee: ₱2,500 (free for life if you apply and get approved by February 29, 2024)

- Interest rate: 3%

- Late payment fee: ₱1,500

- Overlimit fee: ₱1,500

- Cash advance fee: ₱200 per transaction

✅ UnionBank Rewards Credit Card Application Requirements

- Minimum monthly income: ₱15,000

- At least 18 years old

- Valid government-issued ID with photo and signature

- Proof of income (ITR, certificate of employment, etc.)

Start your credit card journey on a rewarding note with the UnionBank Rewards Visa Platinum. With this card, you earn 1 never-expiring point for every ₱30 spend.

If you're an avid shopper or foodie, you get triple the rewards! Earn 3x points when you shop and dine here and abroad.

On top of that, you'll enjoy plenty of UnionBank credit card promos.

🎁 Free Gift from Moneymax: E-Gift, Wireless Earbuds, or Headphones

Eligible card: Any UnionBank credit card

Promo period: Until April 30, 2024

Get a pair of Apple AirPods 2 worth ₱8,490, a JBL Tune 720BT worth ₱4,699, or a Giftaway eGift worth ₱4,000! Just apply for any UnionBank credit card via Moneymax, get approved within the promo period, and then meet the ₱10,000 spend requirement within 60 days from your card approval date.

This Moneymax UnionBank welcome gift promo runs until April 30, 2024 only. Per DTI Fair Trade Permit No. FTEB-187582 Series of 2024.

Note: The promo is exclusive to carded applicants who do not have an existing principal credit card issued by UnionBank and/or Citi.

Metrobank Titanium Mastercard®

📌 Metrobank Titanium Mastercard® Features and Benefits

- 1 point for every ₱20 spend

- 2x rewards points on dining, department store, and online expenses

💳 Metrobank Titanium Mastercard® Fees and Charges

- Annual fee: ₱2,500

- Interest rate: 3%

- Late payment fee: ₱1,000

- Over credit limit fee: ₱750

- Cash advance fee: ₱200 per transaction

✅ Metrobank Titanium Mastercard® Application Requirements

- Minimum monthly income: ₱15,000 if with existing credit card; ₱29,166 if none

- At least 18 years old

- Valid TIN, SSS or GSIS Number

- Business/residence/mobile number

- Proof of income (ITR, certificate of employment, etc.)

Start your credit card rewards journey early with the Metrobank Titanium Mastercard®. Earn 1 point for every ₱20 spend. Double the points for dining, department store, and online expenses.

Read more: Don’t Miss Out on These 17 Metrobank Credit Card Promos This 2024

🎁 Free Gift from Moneymax: ₱2,500 eGift, Dolce Gusto Piccolo XS, or JBL Wave Beam True Wireless Earbuds

_1200x350.jpg?width=734&height=214&name=Metrobank_CC_eGift_JBL_Dolce_Gusto_Piccolo_XS_(Mar_2024)_1200x350.jpg)

Eligible cards: Metrobank Titanium Mastercard®, Platinum Mastercard®, and World Mastercard®

Promo period: Until April 30, 2024

How do you get a Metrobank credit card welcome gift? Simple! Just apply and get approved for any eligible card through the Moneymax website.

Choose between a ₱2,500 eGift voucher via Giftaway, a Dolce Gusto Piccolo XS worth ₱5,199, or a JBL Wave Beam worth ₱3,799 as your free special gift.

This Moneymax Metrobank eGift/Dolce Gusto/JBL promo runs until April 30, 2024 only. So hurry and apply now!

Per DTI Fair Trade Permit No. FTEB-187470 Series of 2024. Terms and conditions apply.

Note: Applicant must be an existing credit cardholder in good standing for at least nine months.

Security Bank Gold Mastercard

📌 Security Bank Gold Mastercard Features and Benefits

- 1 rewards point for every ₱20 spend

- Secure online shopping with SecureCode

- Exclusive rewards and promos all year round

💳 Security Bank Gold Mastercard Fees and Charges

- Annual fee: ₱2,500

- Interest rate: 3%

- Late payment fee: ₱1,000 or unpaid minimum amount due, whichever is lower

- Overlimit fee: ₱500 per occurrence

- Cash advance fee: ₱200 per transaction

✅ Security Bank Gold Mastercard Application Requirements

- Minimum monthly income: ₱30,000

- 21 to 65 years old

- Government-issued photo-bearing ID

- Home and/or office landline number and email address

- Proof of income

If you're a credit card beginner who frequently shops online, consider the Security Bank Gold Mastercard. Enjoy safe shopping with SecureCode, a security feature that requires a one-time password every time you make online transactions. What's more, you can easily rack up rewards points with 1 point for every ₱20 spend!

Read more: Secure These Deals: 15 Security Bank Credit Card Promos for 2024

🎁 Free Gift from Moneymax: ₱2,500 eGift, JBL Bluetooth Speaker, or JBL Wireless Earbuds

-Apr-16-2024-01-32-04-6385-AM.png?width=734&height=214&name=image%20(1)-Apr-16-2024-01-32-04-6385-AM.png)

Eligible cards: Select Security Bank credit cards:

Promo period: Until May 31, 2024

Want a credit card from Security Bank? You're in for a treat if you apply and get approved for an eligible card through Moneymax and meet the minimum spend requirement. Pick your free Security Bank welcome gift: a ₱2,500 Giftaway eGift voucher, a JBL Horizon 2 Bluetooth Clock Radio Speaker worth ₱5,354, or JBL Wave Beam True Wireless Earbuds worth ₱3,799.

This Moneymax Security Bank Giftaway/JBL Horizon 2/JBL Wave Beam credit card promo runs until May 31, 2024 only. Apply now!

Per DTI Fair Trade Permit No. FTEB-191158 Series of 2024. Terms and conditions apply.

BPI Rewards Card

📌 BPI Rewards Card Features and Benefits

- 1 BPI point for every ₱35 spend

- Year-round perks from a variety of stores

- Low forex conversion rate of just 1.85%

- Flexible installment plans of up to 36 months

- Travel insurance of up to ₱2 million

💳 BPI Rewards Card Fees and Charges

- Annual fee: ₱1,550 (free for the first year)

- Interest rate: 3%

- Late payment fee: ₱850 or the unpaid minimum amount due, whichever is lower

- Cash advance fee: ₱200 per transaction

✅ BPI Rewards Card Application Requirements

- Minimum monthly income: ₱15,000

- At least 21 years old

- Valid ID

- Proof of income

If you're looking for a straightforward entry-level credit card, check out the BPI Rewards Card. Use it for your daily needs while getting discounts and earning rewards points in the process. Then use these points to redeem airline miles, shopping credits, and gift vouchers.

Read more: Big Deals With BPI: Top BPI Credit Card Promos This 2024

Petron BPI Card

📌 Petron BPI Card Features and Benefits

- 3% rebate on fuel

- Free ₱200 fuel voucher for first-time cardholders

- Low forex conversion rate of just 1.85%

- Flexible installments at partner stores

- Credit limit to cash for emergencies

💳 Petron BPI Card Fees and Charges

- Monthly fee: ₱1,550 (free for the first year)

- Interest rate: 3%

- Late payment fee: ₱850 or the unpaid minimum amount due, whichever is lower

- Cash advance fee: ₱200 per transaction

✅ Petron BPI Card Application Requirements

- Minimum monthly income: ₱15,000

- At least 21 years old

- Valid ID

- Proof of income

The Petron BPI Card is perfect for young professionals who drive to work. Earn a 3% rebate on fuel (maximum of ₱15,000 per year). Plus, avail of a free ₱200 fuel voucher if you're a first-time cardholder.

BPI Edge Card

📌 BPI Edge Card Features and Benefits

- 1 BPI Point for every ₱50 spend

- Low forex conversion rate of just 1.85%

- Flexible installments at partner stores

💳 BPI Edge Card Fees and Charges

- Monthly fee: ₱110 (free for the first year)

- Interest rate: 3%

- Late payment fee: ₱850 or the unpaid minimum amount due, whichever is lower

- Cash advance fee: ₱200 per transaction

✅ BPI Edge Card Application Requirements

- Minimum monthly income: ₱15,000

- At least 21 years old

- Valid ID

- Proof of income

The BPI Edge Card is perfect for young professionals who want to get the most out of their purchases. Earn 1 rewards point for every ₱50 spend and avail of exclusive deals all year round. Also, enjoy shopping online or abroad, thanks to BPI's forex conversion rates, one of the lowest in the market.

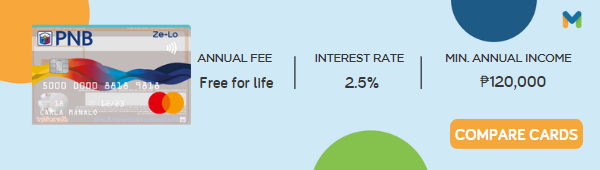

PNB Ze-Lo Mastercard

📌 PNB Ze-Lo Mastercard Features and Benefits

- No late payment fees, annual fees, and overlimit fees

- No annual fee for life for all supplementary cardholders

- Low finance charge

💳 PNB Ze-Lo Mastercard Fees and Charges

- Annual fee: No annual fee for life

- Interest rate: 2.5%

- Late payment fee: None

- Overlimit fee: None

✅ PNB Ze-Lo Mastercard Application Requirements

- Minimum monthly income: ₱10,000

- 21 to 65 years old

- Employed: Certificate of Employment or ITR, valid IDs with signature, proof of billing (for those who don’t have an account with PNB)

- Self-employed: Latest ITR, audited financial statements, valid IDs, and proof of billing

- Foreign nationals: Alien Certificate of Residence, valid passport, and proof of billing, etc.

PNB Ze-Lo Mastercard lets you enjoy numerous perks for fewer fees. It's the perfect credit card for beginners—you won't have to pay a single centavo for late payments, annual fees, and overlimit occurrences with this card.

PNB Visa Classic

.png?width=600&height=170&name=PNB%20Visa%20Classic%20(1).png)

📌 PNB Visa Classic Features and Benefits

- 1% rebate on your revolved interest

- Secure spending with Card Protect

- 0% interest on installment purchases for up to 24 months

💳 PNB Visa Classic Fees and Charges

- Annual fee: ₱300 (free for the first year)

- Interest rate: 3%

- Late payment fee: ₱1,000 or the unpaid minimum amount due, whichever is lower

- Overlimit fee: ₱500

✅ PNB Visa Classic Application Requirements

- Minimum monthly income: ₱10,000

- 21 to 65 years old

- Valid ID

- Employed: Certificate of Employment or ITR, valid IDs with signature, proof of billing (for those who don’t have an account with PNB)

- Self-employed: Latest ITR, audited financial statements, valid IDs, and proof of billing

This PNB credit card is one of the ideal credit cards for beginners because of its low annual fee and required monthly income of only ₱10,000. It's also a good credit card for shoppers, as the card comes with safety features and installment perks.

RCBC Flex Visa

📌 RCBC Flex Visa Features and Benefits

- 2x rewards in two preferred spending categories

- Travel insurance

- Free Skyview Airport Lounge access

- 0% interest on installment purchases for up to 36 months

💳 RCBC Flex Visa Fees and Charges

- Annual fee: ₱1,500 (free for the first year)

- Interest rate: 3%

- Late payment fee: ₱850 or the minimum amount due, whichever is lower

- Overlimit fee: ₱600

✅ RCBC Flex Visa Application Requirements

- Minimum monthly income: ₱15,000

- 21 to 65 years old

- Mobile number and office landline number

- Valid ID

- For employed: Latest ITR/Latest one-month payslip/Certificate of Employment issued within the last six months

- For self-employed: Latest ITR/audited financial statement

Ideal for traveling millennials, the RCBC Flex Visa card comes with usual perks like travel insurance and airport lounge access. It allows users to earn rewards points faster in two out of four spending categories (dining, clothing, transportation, or travel).

You can choose to double your credit card rewards in different categories per billing cycle, making it a convenient option to consider when looking at the best credit cards for beginners.

See also: Save Big on Your Travels With These Agoda Credit Card Promos

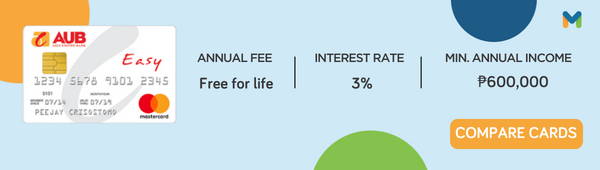

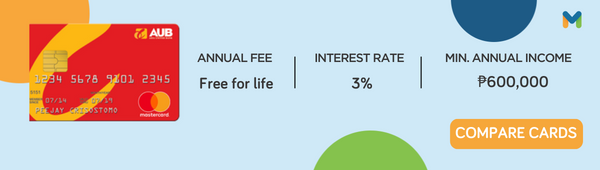

AUB Easy Mastercard and Classic Mastercard

📌 AUB Easy and Classic Mastercard Features and Benefits

- Choose your preferred payment frequency, due date, and minimum payment due

- 1 rewards point per ₱50 spend

💳 AUB Easy and Classic Mastercard Fees and Charges

- Annual fee: No annual fee for life

- Interest rate: 3%

- Late payment fee: ₱250 (weekly payment option) / ₱500 (semi-monthly payment option) / ₱1,000 (monthly payment option) or the unpaid minimum amount due, whichever is lower

- Overlimit fee: None (transactions are declined once the credit limit is exceeded)

✅ AUB Easy and Classic Mastercard Application Requirements

- Minimum monthly income: ₱50,000

- 21 to 65 years old

- At least one year of regular employment status/profitable business operation/professional practice

- Valid ID

- For employed: Latest ITR/Certificate of Employment/one-month pay slip

- For self-employed: Latest ITR (BIR Forms 1701 and 1701Q)/financial statements/DTI business name registration

Although it has a relatively steeper minimum income requirement, AUB's Easy Mastercard is exactly what its name implies: it's easy on the pocket with its no-annual-fee-for-life offer and flexible payment due date options.

The AUB Classic Mastercard also offers waived annual fees for life. Compared to the AUB Easy Mastercard, this credit card's only difference is that it has more minimum amount due options.

Read more: Moneymax Reviews: Comparing AUB’s Budget-Tier Credit Cards

EastWest Privilege Classic Mastercard

📌 EastWest Privilege Classic Mastercard Features and Benefits

- 1 Rewards Point for every ₱100 spend

- Year-round discounts and deals at partner merchants

- Accepted in over 46 million establishments in more than 200 countries

💳 EastWest Privilege Classic Mastercard Fees and Charges

- Annual fee: ₱1,500

- Interest rate: 3%

- Late payment fee: ₱1,500

- Overlimit fee: ₱500

- Cash advance fee: ₱200 per transaction

✅ EastWest Privilege Classic Mastercard Application Requirements

- Minimum monthly income: ₱15,000

- At least 21 years old

- Mobile number and office landline number

- Valid government-issued ID with photo and signature

- Proof of income (ITR, certificate of employment, etc.)

This EastWest credit card is a good choice for first-time cardholders who want a basic card that still lets them earn rewards on their transactions. With an EastWest Privilege Classic Mastercard, you can earn rewards at 1 point per ₱100 spend.

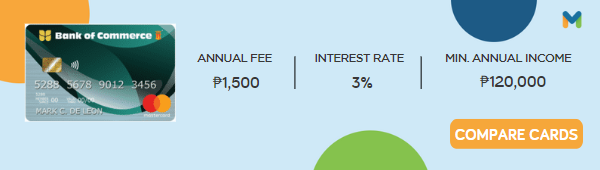

Bank of Commerce Classic Mastercard

📌 Bank of Commerce Classic Mastercard Features and Benefits

- 1 rewards point for every ₱25 spend

- Up to 5x points on shopping and dining spend

- 0% installment up to 36 months

💳 Bank of Commerce Classic Mastercard Fees and Charges

- Annual fee: ₱1,500

- Interest rate: 3%

- Late payment fee: ₱1,000 or the unpaid minimum amount due, whichever is lower

- Overlimit fee: ₱500 per occurrence

- Cash advance fee: ₱200 per transaction

✅ Bank of Commerce Classic Mastercard Application Requirements

- Minimum monthly income: ₱10,000

- 21 to 65 years old

- Valid ID

- Home or office landline number and postpaid mobile number

- For employed: Latest ITR/latest three-month pay slips/Certificate of Employment

- For self-employed: Copy of business papers plus latest audited financial statement/latest ITR/Bank Statement

- For professionals: Latest ITR plus latest audited financial statement/bank statement

- For foreign residents: Proof of income or employment, Deed of Assignment, and Original Comfort Letter plus Special Investor’s Resident Visa/Visa issued by PEZA/Certified True Copy of Passport/Certified True Copy of Alien Certificate of Registration or Work Permit

If you want the best credit card for beginners, the Bank of Commerce Classic Mastercard makes an ideal choice. BankCom charges a relatively low annual fee on this card, so you can save money in the process. Plus, you can earn points quickly through its generous rewards program!

China Bank Prime Mastercard

📌 China Bank Prime Mastercard Features and Benefits

- 1 rewards point for every ₱25 spend at standard merchants or ₱200 spend at service merchants

- All-virtual card for online purchases

- Free annual fee for the first year

💳 China Bank Prime Mastercard Fees and Charges

- Annual fee: ₱1,500 (free for the first year)

- Interest rate: 3%

- Late payment fee: ₱750 or the unpaid minimum amount due, whichever is lower

- Overlimit fee: ₱500 per occurrence

✅ China Bank Prime Mastercard Application Requirements

- Minimum monthly income: ₱20,833

- 21 to 65 years old

- Valid ID

- Existing/active credit card for at least 12 months

- Valid email address, mobile, and landline number

- For employed: Latest three months' payslips/original Certificate of Employment/latest BIR Form 2316

- For self-employed: Latest audited financial statements and BIR Form 1701

- For embassy employees/non-immigrants: Alien Certificate of Registration (ACR) or I-Card (ICR), photocopy of valid passport or visa

Are you a frequent shopper? If yes, then the China Bank Prime Mastercard is a good choice for you. You get a companion virtual card for safe online shopping and a complimentary China Bank-SMAC membership. Plus, you earn 1 rewards point for every ₱25 qualified spend.

China Bank Freedom Mastercard

📌 China Bank Freedom Mastercard Features and Benefits

- 1 rewards point for every ₱20 spend

- Perpetually waived membership fees

💳 China Bank Freedom Mastercard Fees and Charges

- Annual fee: Free for life

- Interest rate: 3%

- Late payment fee: ₱750 or the unpaid minimum amount due, whichever is lower

- Overlimit fee: ₱500 per occurrence

✅ China Bank Freedom Mastercard Application Requirements

- Minimum monthly income: ₱20,833

- 21 to 65 years old

- Valid ID

- Existing/active credit card for at least 12 months

- Valid email address, mobile, and landline number

- For employed: Latest three months' payslips/original Certificate of Employment/latest BIR Form 2316

- For self-employed: Latest audited financial statements and BIR Form 1701

- For embassy employees/non-immigrants: Alien Certificate of Registration (ACR) or I-Card (ICR), photocopy of valid passport or visa

If you want to enjoy perks and rewards even as a first-time cardholder, check out China Bank Freedom Mastercard. Use your card to pay for purchases and earn one point for every ₱20 spend.

The best part? Your annual fees are perpetually waived!

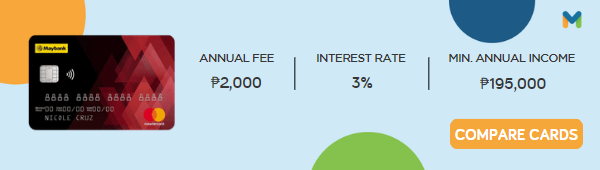

Maybank Standard Mastercard

📌 Maybank Standard Mastercard Features and Benefits

- 0% interest on installment terms with EzyPlans

- Installment plan options for retail transactions and outstanding balances

💳 Maybank Standard Mastercard Fees and Charges

- Annual fee: ₱2,000 (free for the first year)

- Interest rate: 3%

- Late payment fee: ₱850 or unpaid minimum amount due, whichever is lower

- Overlimit fee: ₱750

- Cash advance fee: ₱200 per transaction

✅ Maybank Standard Mastercard Application Requirements

- Minimum monthly income: ₱16,250

- 21 to 65 years old

- Valid IDs

- Employed: Latest ITR/latest pay slips/Certificate of Employment

- Self-employed: Latest ITR/audited financial statements

Make hassle-free transactions wherever you are in the world with Maybank Standard Mastercard. This entry-level credit card is accepted in over 270 countries and 20 million locations.

Secured with EMV-compliant chips and one-time password security measures, Maybank Standard Mastercard is your safe payment partner for online transactions.

Final Thoughts

Credit cards are useful tools. These credit cards for beginners in the Philippines will enable you to build your credit, which will help you in applying for loans and mortgages in the future.

As long as you pay the full balance each month and avoid hidden charges, you’re on the right track to getting your first credit card. More importantly, always compare credit cards to get the best card for your spending needs.

Looking for more options? Click the banner below to get started.

Source: [1] Official PCI Security Standards Council Site

Back to Blog

Back to Blog