Congratulations on deciding to get a life insurance plan! Being insured means sparing your loved ones from financial burden in case something unexpected happens to you.

When life throws a curveball, you can lose your investments. Your savings can also run dry. An accident, permanent disability, critical illness, or death can quickly wipe out everything you’ve worked hard to achieve. So it just makes sense to know your options and get the best life insurance in the Philippines.

But before you sign up for a policy, compare life insurance options just like you would credit cards and other financial products. You'll be spending your hard-earned money on insurance, so make sure your choice is worth paying for.

Why Compare Life Insurance Products?

What is life insurance, and why are there so many options out there? How much is life insurance, and how do you know if you’re paying too little or too much?

For the uninitiated, life insurance can be a confusing and complex topic. This is why it pays to do your own legwork. Aside from learning how life insurance works and which companies offer the best life insurance in the Philippines, you must identify your needs.

Before you speak with a financial advisor, shop around, compare your choices, and assess the results. Your goal is to find a policy that meets your needs and budget, specifically one with the most coverage at the least possible cost. Narrow your choices by comparing insurance companies, types, and policies.

How to Choose the Best Life Insurance in the Philippines

First, make sure that the insurance company you choose won’t likely fold in five or 10 years. Also, look for these three essential qualities when comparing life insurance providers.

Things to Consider When Choosing a Life Insurance Company

✔️ Licensed to Operate in the Philippines

Check the Insurance Commission’s list of licensed insurance firms[1] to see if the companies you’re considering are legitimate.

✔️ Solid Company Background

If an insurance firm has been operating steadily for a long time with a good reputation in the industry, then you know it’s worth trusting. Visit the website of insurance providers to check their company background.

✔️ Strong Financial Performance

The best life insurance firms perform well based on the Insurance Commission's five criteria.

- Premium Income - This is the total amount a company receives from its clients’ premiums. It’s also a good indicator of an insurance firm’s financial strength, as a higher premium income means it serves a lot of policyholders.

- Assets - An insurance company's assets include all its properties that are available to use for paying its debts. The higher a firm's assets, the better it can manage its debt repayments.

- Net Worth - This is the value of all the company’s assets minus all its liabilities. So an insurance firm with a higher net worth can better withstand financial crises, as it has enough assets to enable its business to operate despite losses.

- Net Income - The net income is computed by deducting a company's total expenses from its total revenues. This financial performance indicator is different from the premium income, as the net income reflects the actual income that the company is earning from its business.

- New Business Annual Premium Equivalent (NBAPE) - The Insurance Commission uses this metric to measure and compare the life insurance revenue of insurance companies' newly issued policies within the calendar year. It's the sum of the total of actual first-year (regular) premiums plus 10% of single premiums.

Best Life Insurance Companies in the Philippines

What is the number one insurance company in the Philippines? Here's the Insurance Commission's latest ranking of life insurance companies in the Philippines, based on premium income, assets, net worth, net income, and new business annual premium equivalent.

Note: Data below are as of December 31, 2022, based on the latest statistics from the Insurance Commission's official website.

👉 Life Insurance Companies with Highest Premium Income

Premium income is the revenue an insurer earns from payments from policyholders.[2] Sun Life of Canada[3] holds the top spot in this category.

👉 Largest Life Insurance Companies Based on Assets

As far as assets go, Sun Life also ranks number one in terms of total assets,[4] followed by AIA and Philippine AXA Life.

👉 Life Insurance Companies with Highest Net Worth

Net worth is the value of the assets a corporation owns, minus the liabilities they owe.[5] It’s one of the metrics you can refer to if you want to check an insurance company’s financial health and current financial position. AIA is in the top spot in this category, followed by Insular Life.[6]

👉 Life Insurance Companies with Highest Net Income

To calculate an insurance company's net income, get the total sales and deduct the cost of goods sold, selling, general and administrative expenses, operating expenses, depreciation, interest, taxes, and other expenses.[7] You can also check the life insurance company’s net income if you want to learn more about its profitability.

Sun Life ranked number one in this category, with AIA Philippines coming in second.[8]

👉 Life Insurance Companies with Highest NBAPE

The New Business Annual Premium Equivalent (NBAPE) measures and compares the life insurance revenue of new business within the calendar year by life insurance companies. For this category, Sun Life holds the number one spot.[9]

What is the Best Life Insurance Type for Me?

What type of life insurance should you get? This is a significant consideration, so compare different types of life insurance in the Philippines and the insurance protection it offers before making that purchase.

Life Insurance Considerations

To determine the best life insurance policy in the Philippines that’s suitable for your goals and needs, consider the following factors:

- The insurance coverage you need

- How long you want to be insured

- How much you are willing and can afford to pay in premiums

- Whether you want protection only or have additional savings in your insurance policy

Read more: Should You Get Life Insurance? Consider These 8 Factors

Types of Life Insurance in the Philippines

Here are your different options for insuring yourself and your family.

👉 Term Life Insurance

What is term life insurance? This type of life insurance provides protection over a specific time frame, ranging from one to over 10 years. Death benefits are paid to survivors if the insured’s death occurs within the policy period. If you outlive the term period, your coverage ends, and you’ll get nothing back.

As a pure form of insurance, term insurance has no savings component, making it the least expensive type. Term life insurance in the Philippines is ideal for low-income earners who cannot afford whole life insurance but want maximized protection at a minimal cost.

If you want options for the best term insurance in the Philippines, check out Manulife YRT or React5, AIA Guardian, PRULife Your Term, or Sun Safer Life.

👉 Whole Life Insurance

Unlike term insurance, whole life insurance provides protection for your entire life or until you’re 100. When you get whole life insurance in the Philippines, your beneficiaries won’t just receive the death benefits—you can enjoy the savings component in cash values and dividends as well. You can benefit from the savings component while you’re still alive to fund your retirement or your child’s college education.

👉 Prepaid Health Cards

Unlike other health insurance types, this one is a little more special. Similar to an e-voucher, a prepaid health card allows you to avail of a one-time visit to selected medical facilities and specific treatments depending on your card.

In general, three types of prepaid cards come with any of the following coverage:

- Emergency care

- Hospitalization

- Preventive care

Prepaid health cards are the more affordable and flexible option compared to regular health insurance. However, they have fewer services and typically expire after one year.

👉 Variable Universal Life (VUL) Insurance

VUL insurance combines whole life insurance and investment. Death benefits are paid to survivors anytime the insured dies. Its accumulated cash value is invested in balanced funds, bonds, money market funds, and/or equity funds. Thus, VULs are ideal for long-term investment and insurance needs.

Best Life Insurance with Investment in the Philippines

📌 Singlife Protect Your Goals

Do you work hard for your goals but worry about not having enough money for your or your family's future? Are you determined to continuously grow your savings?

With Singlife's Protect Your Goals, an investment-linked insurance product that's accessible digitally through the Singlife Plan & Protect App, you can simultaneously invest to grow your money and enjoy insurance coverage. For as low as ₱500, you can finally start taking control of your finances and achieve your major life goals.

_CTA_Banner.png?width=751&height=219&name=Singlife_Main_KV_(Sep_2023)_CTA_Banner.png)

Singlife Protect Your Goals Features:

- Access the VUL product and manage your policy via the Singlife Plan & Protect App in just a few taps

- Can start investing with only ₱500

- Investment in professionally managed funds

- Auto-invest feature for continuous investments

- Life insurance coverage: The bereaved family will receive benefits worth 125% of the insured's total payments

- No entry fees: 100% of your money is invested, so you can make the most out of your investment

- No lock-in periods, so you can pause or withdraw anytime

📌 FWD Set for Life

If you’re set on getting lifetime protection and investing your money for your children’s education, future business, or your own retirement, you can opt for the FWD Set for Life plan. You can purchase this FWD life insurance as a stand-alone plan or customize it with other FWD insurance products.

FWD Set for Life Features:

- Lifetime protection and investment product to build your wealth

- Coverage up to 100 years old

- Loyalty bonus on your policy’s 10th year and every five years after that

- Waived future payments if diagnosed with critical illness or permanent disability

- Available add-ons to customize your coverage

- Additional cash benefit for accidental death before age 75

📌 FWD Family Hero

Another FWD life insurance product that offers lifetime protection and helps you create passive income and build your wealth is the FWD Family Hero. Aside from the life insurance coverage and investment component, it protects you and your loved ones from unexpected health setbacks.

FWD Family Hero Features:

- Consists of Set for Life or Manifest for life insurance and investment

- Provides critical illness protection via HealthPro

- Offers hospital cash benefit via RecoveryPro (₱1,000 to ₱10,000 per day and 100% more if confined in the ICU)

- Waived future premiums for the insured for major illness, permanent disability, or loss of life

Related reading: FWD Life and Security Bank tie up for insurance

📌 Sun Maxilink Prime

If you're looking for life insurance with an investment component, check out Sun Maxilink Prime, offered by Sun Life Insurance in the Philippines. It provides life insurance coverage while growing your money, which you can use to fund your long-term goals or any emergency.

Sun Maxilink Prime is a suitable investment-linked life insurance product whether you’re starting a family, planning for your retirement, or leaving a legacy for your loved ones.

Sun Maxilink Prime Features:

- Investment-linked life insurance plan

- Guaranteed life insurance benefit (at least twice the face amount for untimely deaths)

- Supplemental benefits and riders for added protection

- Flexible investment options

- Partial fund withdrawals during emergencies

- Manageable payments

- Loyalty Bonus when you keep your policy active for at least 10 years

📌 PRULink Assurance Account Plus

Looking for the best whole life insurance in the Philippines? Check out the PRULink Assurance Account Plus. It’s an investment-linked life insurance plan that provides maximum protection while helping you achieve financial growth.

PRULink Assurance Account Plus Features:

- High protection at affordable premiums (annual premiums start at ₱20,000)

- Coverage up to 100 years old

- Eligible for applicants up to 70 years old

- Option to add more benefits for increased protection

- No charges for fund withdrawals

- Loyalty bonus

📌 Manulife Freedom

Manulife's life insurance products in the Philippines also offer investment options. Manulife Freedom helps you save for the future and gives you guaranteed payouts and a lump sum.

Manulife Freedom Features:

- Guaranteed cash values and lump sum benefit

- Life insurance coverage up to age 65

- Dividend earnings

- Added benefits with your savings

- Payable in five or 10 years

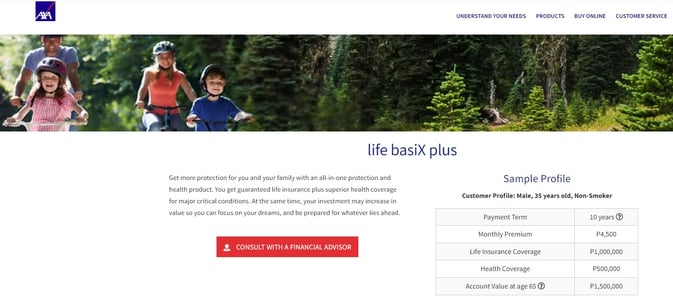

📌 AXA Life BasiX Plus

This is a life insurance, health insurance, and investment product from the Philippine AXA Life Insurance Corporation. With this insurance and investment package, you can focus on building your wealth and preparing for anything the future holds.

AXA Life BasiX Plus Features:

- Guaranteed life coverage starting from ₱1 million

- Guaranteed medical fund when diagnosed with any of the covered major critical illnesses

- Partial withdrawals of health coverage starting at age 70

- At least 10 years of payment to build your fund, with an option to pay longer to increase your investment

- Optional riders for more comprehensive coverage

📌 AIA Family Secure

Family Secure is a life insurance plan that allows you to live a life free of worry. It provides high-value life insurance coverage that you can convert into a retirement plan when you get older, with a minimum premium of ₱16,000 a year.

AIA Family Secure Features:

- High-value life insurance

- Convertible to a retirement plan (decrease your coverage to boost your account value)

- Exclusive Philam Vitality rewards and perks

- Customizable plan to increase coverage

- Issue age up to 70 years old

- Coverage age until 100 years old

Related reading: Personal Accident Insurance: What is It and Where to Get One?

5 Tips on Life Insurance Comparison in the Philippines

Once you’ve chosen your top insurance companies and the right insurance type, it’s time to compare life insurance policies.

Here are several tips to help you pick the best life insurance in the Philippines:

- Ask for life insurance rates, quotes, or proposals for your preferred insurance coverage from two or three providers of your choice. For the same coverage, benefits and premiums may vary among insurance companies.

- Compare benefits and riders. Evaluate which primary and supplementary benefits are suitable for your insurance needs and which ones you can do without. For example, decide whether to include critical illness benefits in your life insurance plan.

- Compare premiums. For the same coverage, some policies are more expensive than others. For example, a policy may have a higher premium because it’s designed for a higher retirement fund. Ask your insurance advisor about the reasons for the price differences.

- Thoroughly review the fine print. Check the life insurance charges and fees—such as taxes, policy fees, and rider charges—that will be deducted monthly from your total funds.

- Ask a lot of questions. If something is unclear, make sure to ask questions. Discuss each policy feature with your insurance advisor. Probe into what would happen in different scenarios in the future. Get all bases covered rather than regret your decision later.

Final Thoughts

So which life insurance is right for you? The best life insurance in the Philippines should offer a product consistent with your life goals and the best overall value for your money.

How much life insurance costs in the Philippines also varies depending on one's age and health condition.

Before applying for a life insurance plan, compare insurance companies, types, and insurance policies first to get the best package. Once you've chosen a policy, pay your insurance premiums easily with a credit card.

In case you don't have one yet or need another one, use Moneymax to find the perfect credit card for you. Check out a few options below:

| Credit Card | Bills Payment Perks |

|

HSBC Red Mastercard

|

|

|

Security Bank Complete Cashback Mastercard

|

|

|

BPI Amore Cashback Card

|

|

|

AUB Easy Mastercard

|

|

Sources:

- [1] Insurance Commission’s list of licensed insurance firms

- [2] Premium Income (Investopedia, 2022)

- [3] Premium Income of Life Insurance Companies as of December 31, 2022

- [4] Assets of Life Insurance Companies as of December 31, 2022

- [5] Net Worth: What It Is and How to Calculate It (Investopedia, 2023)

- [6] Net Worth of Life Insurance Companies as December 31, 2022

- [7] Net Income Definition: Uses, and How to Calculate It (Investopedia, 2022)

- [8] Net Income of Life Insurance Companies as December 31, 2022

- [9] New Business Annual Premium Equivalent (NBAPE) of Life Insurance Companies as December 31, 2022

Back to Blog

Back to Blog